The impact of inflation on the personal finances of Americans

Understanding the Impact of Inflation on Personal Finances

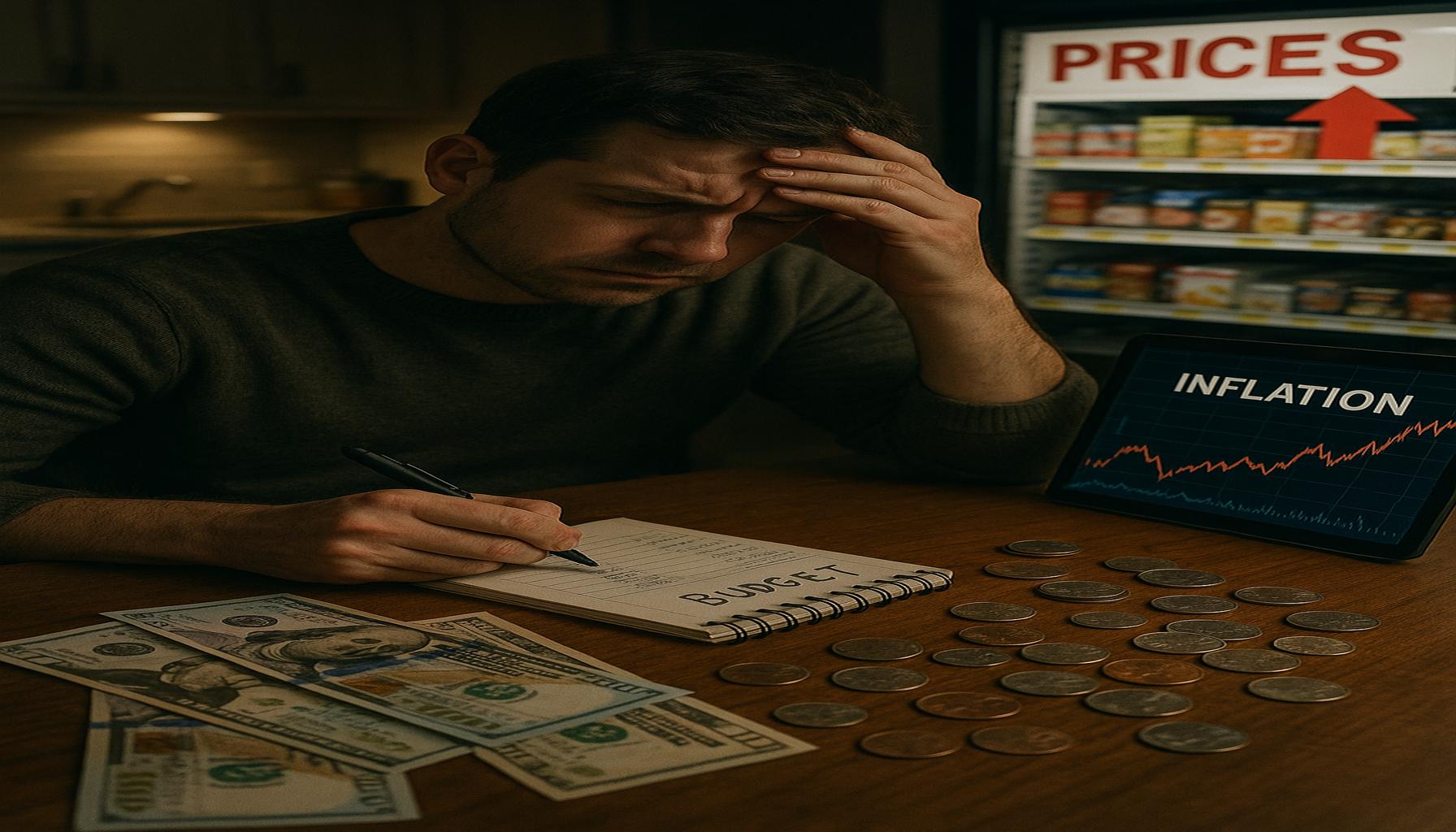

Inflation is an essential concept that affects nearly every facet of personal finances. As the prices of goods and services rise, the value of money diminishes, making it crucial for individuals to understand how inflation can change their financial landscape. The erosion of purchasing power means that consumers must increasingly rethink their spending habits, savings strategies, and investment decisions.

Key Areas Affected by Inflation

One of the most immediate consequences of inflation is the increase in the cost of living. Essentials like food, housing, and transportation can see significant price hikes. For example, a staple item like a loaf of bread, which might have cost $2 last year, could jump to $2.50 this year. For families, this incremental increase can lead to a major shift in budgeting as more income is directed toward basic needs, leaving less for discretionary spending or savings.

Interest rates also see adjustments in response to inflationary trends. When inflation rises, the Federal Reserve may increase interest rates in an effort to curb spending and stabilize prices. This change can affect everything from the interest on loans, such as mortgages and personal loans, to credit card rates. If you have a credit card with a variable interest rate, for example, a rise in interest rates can mean higher monthly payments, straining finances even further.

The impact of inflation is keenly felt in savings and investments. If the inflation rate surpasses the interest rate earned on savings accounts, the real value of those savings diminishes over time. For instance, if you have $1,000 in a savings account earning 1% interest, but inflation rises to 3%, the purchasing power of your savings effectively decreases. Consequently, individuals must seek out investments that ideally outpace inflation, such as stocks, real estate, or inflation-protected securities.

The Pressure of Inflation on Different Demographics

Not everyone feels the effects of inflation equally. Low-income families often bear a heavier load since they spend a larger portion of their income on necessities. For instance, if the price of gasoline rises, they might have no option but to cut back on other expenses to afford transportation, which in turn can impact their ability to find work.

Retirees living on fixed incomes face unique challenges as prices rise. If a retiree’s pension or social security benefits do not increase in line with inflation, they may find it increasingly difficult to cover essential expenses like healthcare and housing.

Moreover, young professionals entering the workforce may also find inflation exacerbating their financial struggles, especially if they already carry student loan debt. Rising living costs could make it hard for them to save for future goals like buying a home or investing in their retirement.

Strategies to Manage Inflation’s Impact

Understanding the implications of inflation on personal finances can empower individuals to make more informed financial choices. It is essential for consumers to create budgets that account for rising costs, explore investment options that provide a hedge against inflation, and consider ways to increase income, such as side jobs or developing new skills. By staying informed and proactive, individuals can better navigate the complexities of inflation and maintain their financial health.

DIVE DEEPER: Click here to learn more

The Financial Ripple Effect of Inflation

Understanding how inflation impacts personal finances is vital for every American. As inflation climbs, the cost of everyday essentials escalates, impacting household budgets in various ways. This shift is not just confined to the prices of goods, but it reaches into almost every corner of personal finance. By examining the specific areas that inflation affects, individuals can better prepare themselves to manage their financial well-being in challenging economic times.

Rising Costs: The Cost of Living

The most visible effect of inflation is the increased cost of living. As prices soar, daily expenses for necessities such as groceries, rent, and utility bills can strain budgets. For instance, consider a family who finds that their monthly grocery bill has swelled from $600 to $750 over a year. This $150 increase may force them to make difficult decisions about where to cut back, impacting other areas of their financial lives, such as entertainment or emergency savings.

A quick glance at common goods reveals similar trends. An average gallon of milk that costs $3.50 today might edge towards $4.00 in just a few months. These incremental price increases add up quickly, compelling individuals and families alike to examine their spending habits more closely. When essential goods become costlier, thoughtful planning becomes necessary to ensure that spending aligns with available income.

Interest Rates: A Double-Edged Sword

Interest rates are another area significantly influenced by inflation. The Federal Reserve often responds to rising inflation by implementing higher interest rates. For Americans with mortgages, auto loans, or credit card debt, this can mean steeper monthly payments. Consider this: if the Federal Reserve raises rates by 1 percentage point, someone with a $300,000 mortgage could see their monthly payment increase by approximately $175 or more. For many, this added expense can make budgeting even more difficult, leading to financial strain.

Investment Decisions: The Race Against Inflation

Inflation also affects savings and investments. When the inflation rate exceeds the interest rate earned on savings accounts, the real value of those savings diminishes. For example, if you save $5,000 in a bank account earning 0.5% interest, but inflation rises to 2%, the purchasing power of your savings effectively decreases, eroding your financial security. It becomes essential for investors to seek out options that outpace inflation, such as:

- Stocks: Historically, the stock market has offered returns that can outstrip inflation over the long term.

- Real Estate: Property usually appreciates in value over time, providing a potential hedge against inflation.

- Inflation-Protected Securities: These government-issued bonds adjust with inflation rates, ensuring your investment keeps up with rising prices.

By understanding these impacts, individuals can make informed financial decisions that protect their purchasing power and sustain their financial health in the face of rising inflation.

LEARN MORE: Click here to find out how to apply for a Citibank credit card online</

Adapting Financial Strategies in an Inflationary Environment

As inflation continues to challenge the financial landscape, Americans must adapt their financial strategies to remain secure in their personal finances. By being proactive, individuals can navigate rising costs and changing interest rates with greater ease. This involves not only reassessing spending habits but also exploring new avenues to protect and grow wealth effectively.

Smart Spending: Adjusting Budgets

In times of rising inflation, adjusting budgets becomes essential. Families may find that their existing budget no longer aligns with current prices. A useful strategy is to categorize spending into needs and wants. Necessities, such as housing and groceries, should take priority, while discretionary spending on entertainment or dining out can be reassessed.

For example, if a family typically allocated $200 monthly for dining out, it may be time to cut that in half and introduce more home-cooked meals. This adjustment not only saves money but also offers an opportunity to spend quality time together. Keeping track of spending through apps or simple spreadsheets can help individuals spot areas where they can save.

Emergency Savings: A Buffer Against Uncertainty

With prices fluctuating, it becomes increasingly important to maintain a solid emergency fund. Ideally, this fund should cover three to six months of living expenses. Having a buffer can help households weather unforeseen situations, such as medical emergencies or job loss, without resorting to high-interest debt.

For those just starting, setting a goal of saving a small but consistent amount each month can accumulate over time. For instance, setting aside $100 each month could lead to a $1,200 emergency fund in just one year, providing peace of mind amid inflationary pressures.

Debt Management: Taming Interest Costs

As interest rates rise, so too can the costs associated with debt repayment. This reality makes effective debt management critical for maintaining financial health. Americans with variable-rate debts, like credit cards or certain loans, should consider prioritizing aggressive repayment strategies to minimize interest expenses.

One method is the debt avalanche approach, where individuals focus on paying off high-interest debt first while maintaining minimum payments on others. For instance, if a person has two credit cards, one with a 20% interest rate and another with a 12% rate, it makes sense to put extra funds toward the higher-rate card to avoid accumulating more debt over time.

Long-term Investments: Staying Ahead of Inflation

Investment strategies play a significant role in how Americans can safeguard their finances against inflation. It’s critical to recognize that inflation can erode purchasing power, and thus, seeking investments that yield returns that outpace inflation is paramount. Beyond stocks and real estate, individuals can explore options like mutual funds or exchange-traded funds (ETFs) focused on sectors such as commodities and infrastructure, which often perform well during inflationary periods.

Moreover, diversifying investment portfolios with international assets can also provide a hedge against domestic inflation. Exposure to foreign markets may buffer the effects of inflation at home and enhance overall portfolio resilience.

By embracing smart spending habits, expanding emergency savings, strategically managing debt, and exploring robust investment opportunities, Americans can better navigate the challenges posed by inflation and work toward financial stability.

DISCOVER MORE: Click here to learn how to apply

Conclusion

The persistent rise of inflation poses significant challenges to the personal finances of Americans. As purchasing power diminishes and costs fluctuate, it is vital for individuals and families to take control of their financial futures through informed decision-making. By reassessing budgets, prioritizing essential expenses, and being mindful of discretionary spending, Americans can stretch their dollars further. Additionally, establishing and maintaining a robust emergency fund provides a crucial safety net in times of uncertainty.

Effective debt management is paramount as interest rates rise, prompting a need to focus on high-interest debts to avoid unnecessary costs. Engaging in strategic repayment plans, such as the debt avalanche method, can significantly reduce the financial burden over time. Moreover, it is essential to recognize the importance of long-term investments that outpace inflation. Diversifying portfolios beyond domestic assets can enhance resilience against economic shifts.

Ultimately, while inflation can seem daunting, it also serves as a catalyst for positive change in financial habits. By adopting a proactive mindset and implementing these strategies, Americans can not only withstand the pressures of inflation but also lay the groundwork for a more secure financial future. Embracing this opportunity to cultivate financial discipline can lead to improved stability and success, equipping individuals with the tools needed to navigate an ever-evolving economic landscape.