The Influence of Student Loans on Personal Credit

The Financial Commitment of Student Loans

Student loans have become a crucial tool for many aspiring students in New Zealand, facilitating their access to higher education. However, this financial commitment does not come without consequences, particularly impacting one’s personal credit. As the borrowing trend continues to rise, it is essential to examine how these loans influence not just immediate educational opportunities but also long-term financial health.

High Levels of Debt

One of the most significant challenges faced by graduates is the accumulation of substantial debt. According to recent statistics, the average tertiary student loan in New Zealand is approximately NZD 23,000. For many, this amount can create a daunting financial burden once they enter the workforce. For instance, if a graduate earns a starting salary of NZD 50,000, a significant proportion of their income may be allocated towards student loan repayments. This can limit their ability to save for other financial goals, like buying a home or investing in their future.

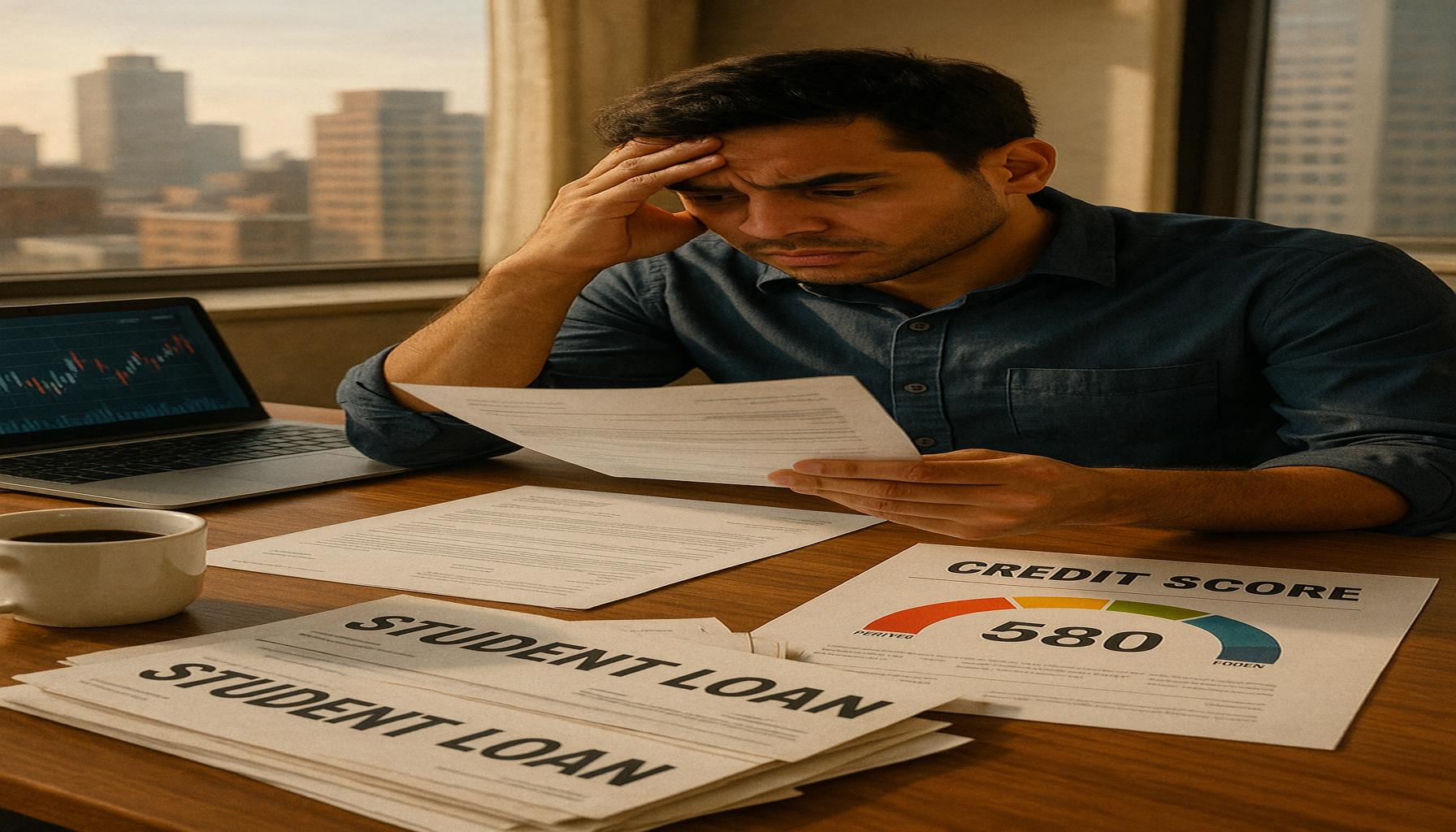

Impact on Credit Scores

Another essential factor to consider is how student loans affect credit scores. Consistently making repayments can enhance a borrower’s creditworthiness, thus improving their credit score over time. For instance, if a graduate pays their loan on time for three consecutive years, this positive behavior could contribute to a more favorable credit profile, allowing them easier access to other forms of credit, such as personal loans or mortgages.

Conversely, missed payments can have significant negative repercussions. A single late payment can lead to a decrease in a credit score, which may hinder one’s ability to secure favorable loan terms in the future. This scenario underscores the importance of developing a sound repayment strategy early on.

Types of Loans and Their Effects

The type of student loan taken also plays a crucial role in shaping one’s credit profile. In New Zealand, the two primary categories are government loans and private loans. Government loans often come with more lenient repayment schemes tied to income levels, which can mitigate the potential negative effects on credit ratings during tough financial times. In contrast, private loans may impose higher interest rates and stricter repayment conditions, which can escalate debt and complicate one’s financial situation.

Guiding Financial Management

By gaining a clear understanding of the relationship between student loans and personal credit ratings, borrowers can make more informed financial decisions. Factors such as selecting the right repayment plan and being mindful of interest rates can significantly influence credit history. Research from recent studies indicates that borrowers who proactively manage their loans—by assessing repayment options and budgeting effectively—tend to fare better in their overall financial stability.

In conclusion, navigating the student loan landscape in New Zealand requires careful consideration and planning. By being aware of the implications student loans have on credit profiles, students and graduates can implement strategies to ensure sound financial health in the long run.

CHECK OUT: Click here to explore more

Understanding the Long-term Effects of Student Loans

The influence of student loans on personal credit extends beyond the immediate burden of repayment. To gain a clearer picture, it’s crucial to analyze how debt repayment behavior and management strategies affect overall credit ratings. This analysis not only benefits graduates but also provides valuable insights for current students navigating their educational financing options.

Debt Repayment Behavior

One of the key determinants of how student loans impact personal credit is the borrower’s repayment behavior. Consistent repayment is essential in fostering a healthy credit profile. A credit score is generally influenced by several factors, including:

- Payment History: This accounts for approximately 35% of a credit score, highlighting the importance of timely payments on all debts, including student loans.

- Credit Utilization: Although this is more commonly associated with credit cards, managing available credit wisely can also apply to loan balances.

- Length of Credit History: Longer credit history often signifies reliability, which is beneficial when it comes to student loan accounts that remain open over time.

- Types of Credit: Having a mix of credit types, such as credit cards and loans, can positively impact a credit score, showing lenders that the borrower can manage various financial products.

To exemplify, a graduate who begins their repayment promptly after graduation and maintains a consistent payment schedule can expect their credit score to improve significantly over time. Conversely, neglecting these obligations or experiencing payment defaults can lead to a marked drop in one’s credit rating, making future borrowing more difficult and expensive.

The Role of Loan Servicers

Another important aspect to consider is the role of loan servicers in managing student loans. In New Zealand, the government’s student loan scheme is administered by the Inland Revenue, which offers various options for repayment strategies. Understanding these options is essential for borrowers, as it can provide room for tailoring repayments based on income levels and financial circumstances. Failure to engage with the servicer may lead to missed opportunities for financial relief, which can adversely affect one’s credit profile.

Strategic Planning for Credit Stability

Further, graduates can take active steps to enhance their credit profiles while managing student loans. Here are several strategies:

- Budgeting: Establishing a monthly budget helps ensure that timely payments for student loans and other debts are accounted for.

- Emergency Savings: Building an emergency fund can prevent defaults during unforeseen financial challenges.

- Periodic Credit Checks: Regularly monitoring credit reports allows borrowers to track changes and address discrepancies quickly.

- Consideration of Additional Forms of Credit: Gradually introducing manageable credit products can demonstrate responsible borrowing behavior, further enhancing credit scores.

Strategies such as these emphasize the proactive management of student loans, which not only stabilizes repayment expectations but can also create a more robust credit profile over time. By recognizing how repaying student loans can influence credit scores, borrowers will be better equipped to make informed financial decisions that secure future opportunities.

SEE ALSO: Click here to read another article

Exploring Alternative Loan Structures and Their Impact on Credit

In addition to repayment behavior, the type of student loan structure significantly influences personal credit outcomes. Distinct loan types such as government-funded loans, private loans, and income-driven repayment plans present varying implications for credit scores. To fully grasp the influence these loans have, it is essential to evaluate each option in terms of flexibility, payment obligations, and their respective effects on personal credit rating.

Government versus Private Student Loans

Government student loans, predominantly available through StudyLink in New Zealand, often come with more favorable terms compared to private loans. For instance:

- Lower Interest Rates: Government loans typically feature lower interest rates, making them less burdensome over time. This reduced financial pressure can lead to improved repayment capabilities and a healthier credit score.

- Flexible Repayment Options: Many government loans offer income-dependent repayment, allowing borrowers to pay a percentage of their income rather than a fixed amount. This flexibility can help avoid default and maintain timely repayments.

In contrast, private loans often present stricter repayment conditions, higher interest rates, and fewer flexible options, potentially leading to increased financial strain. Borrowers with private loans may face challenges in their credit profiles if they fail to meet higher payment requirements, causing spikes in delinquency rates.

Understanding Income-Driven Repayment Plans

Income-driven repayment plans can serve as a beneficial strategy for graduates struggling to manage their loan obligations. Such plans adjust monthly payments based on income, reducing the risk of missed payments that could detrimentally affect credit scores. Research has shown that borrowers on income-driven plans are less likely to default compared to those on standard repayment schedules.

In New Zealand, one prominent scheme available to borrowers is the Loan Repayment Scheme that allows eligible individuals to pay only based on their income levels. This system has proven highly effective, as it not only enables borrowers to align their repayment capabilities with their earning potential but also enhances credit management strategies.

Leveraging Credit Management Services

Beyond understanding loan structures, graduates can also benefit from leveraging credit management services. These agencies provide personalized financial advice and budgeting assistance, helping borrowers navigate their repayment options and credit score enhancements. For instance, utilizing a credit counseling service can equip borrowers with knowledge on:

- Debt Consolidation: Combining multiple loan repayments into a single manageable loan can simplify payment processes and potentially lower interest rates.

- Negotiating Repayment Terms: Engaging with lenders to negotiate more favorable repayment terms can prevent defaults and maintain a healthier credit score.

By understanding the different types of student loans and utilizing available networking opportunities, graduates can devise a comprehensive credit management strategy. Through informed decisions regarding the nature of borrowing and proactive engagement with credit management resources, they can optimize personal credit ratings and establish a pathway toward financial stability long after their education has concluded.

SEE ALSO: Click here to read another article

Conclusion

The intricate relationship between student loans and personal credit cannot be overstated, as it significantly shapes the financial landscape for many graduates. As explored in this article, the type of student loan — whether government-funded or private — plays a pivotal role in influencing credit ratings. Government loans tend to offer lower interest rates and flexible repayment options, which are vital for fostering better credit outcomes. Contrarily, private loans can burden borrowers with higher interest rates and stricter repayment conditions, often leading to detrimental effects on credit scores.

Moreover, income-driven repayment plans serve as an effective mitigation strategy for those grappling with repayment challenges. By linking monthly payments to income, borrowers are less likely to face defaults, thereby protecting their credit profiles. This flexibility highlights the importance of understanding not only the loan structure but also the available repayment options that align with one’s financial situation.

As graduates transition into the workforce, leveraging credit management services can further enhance their financial stability. These resources assist in refining budgeting strategies and negotiating favorable repayment terms, ultimately leading to improved credit health. Overall, navigating the landscape of student loans and their implications on credit is essential for fostering long-term financial well-being. By making informed choices and utilizing strategic financial tools, borrowers in New Zealand can optimize their credit standings and establish a foundation for future financial success.