The Importance of Credit for Young Adults in New Zealand

Understanding Credit in New Zealand

In today’s financial landscape, understanding credit is essential for young adults. Establishing sound credit can influence major life decisions, from renting an apartment to securing a personal loan. Credit is not merely a number; it represents a person’s financial reliability and ability to manage debt. New Zealand’s financial culture increasingly recognizes the importance of credit literacy among young people, reflecting a shift towards a more financially savvy generation.

Credit affects numerous aspects of financial health, including:

- Loan Approval: A good credit score increases the likelihood of being approved for loans. For instance, individuals with a credit score above 700 typically find it easier to obtain mortgages or car loans compared to those with lower scores. If a young adult applies for a home loan, a good credit score can mean the difference between approval and rejection, often with lenders requiring a minimum score for eligibility.

- Interest Rates: Higher credit ratings often result in lower interest rates, saving money over time. According to recent data from the Reserve Bank of New Zealand, a difference of even half a percentage point can lead to substantial savings over the life of a loan. For example, on a $500,000 mortgage term of 30 years, a 0.5% difference in interest can save borrowers over $30,000 in payments.

- Rental Applications: Landlords frequently check credit scores as part of the rental application process. In a competitive rental market, having a higher score can provide an edge over other applicants. A negative mark or a thin credit history can lead to rejection and limit housing options, making it vital for young adults to manage their credit proactively.

Moreover, credit can serve as a foundation for future financial opportunities. Young adults need to be aware of:

- Building Credit Early: Starting to build credit while young can lead to a better financial future. Opening a credit card, secured loan, or even a mobile phone plan can help establish credit history. Census data suggests that when young adults engage with credit products responsibly, they build a solid credit history, which is beneficial when applying for larger loans later in life.

- Common Credit Products: Understanding credit cards, personal loans, and student loans is crucial. Each product comes with its own benefits and pitfalls that can affect overall credit health. For instance, using a credit card wisely, by maintaining low balances and paying off debts on time, can significantly enhance a credit score.

- Managing Debt Responsibly: Avoiding high debt levels can protect and improve credit scores. In a study by the Financial Capability Barometer, New Zealanders aged 18-29 reported high levels of credit card debt. Therefore, developing strategies such as budgeting and prioritizing repayment can mitigate debt, ultimately supporting credit health.

In New Zealand, where financial literacy plays a significant role in economic stability, young adults must prioritize understanding credit. The ability to navigate credit responsibly not only shapes their financial journeys but also empowers them to make informed decisions about their future. By fostering a strong credit foundation, young adults can position themselves for long-term success, enabling them to pursue milestones such as home ownership, investment opportunities, and personal development without the burden of excessive debt.

SEE ALSO: Click here to read another article

The Impact of Credit on Financial Well-being

For young adults in New Zealand, the implications of a healthy credit profile extend deeply into various facets of daily life. A strong credit score not only opens doors to favourable loan terms and housing options but also plays a crucial role in enabling financial security during pivotal life stages. Understanding the mechanisms behind credit ratings can significantly affect how young individuals approach their financial futures.

One critical aspect to consider is the role of credit scores in accessing different types of financial products. The most common credit scoring model in New Zealand ranges from 0 to 1000, with scores over 660 generally considered to be ‘good.’ Here’s how different ranges can affect young adults:

- Excellent (800+): Individuals within this bracket enjoy the best rates and terms on loans, making significant savings on interest, and establishing a reputation that can facilitate easier negotiations with creditors.

- Good (660-799): While still a desirable range, individuals here may see slightly higher interest rates, yet they still stand a reasonable chance of obtaining loans with acceptable terms.

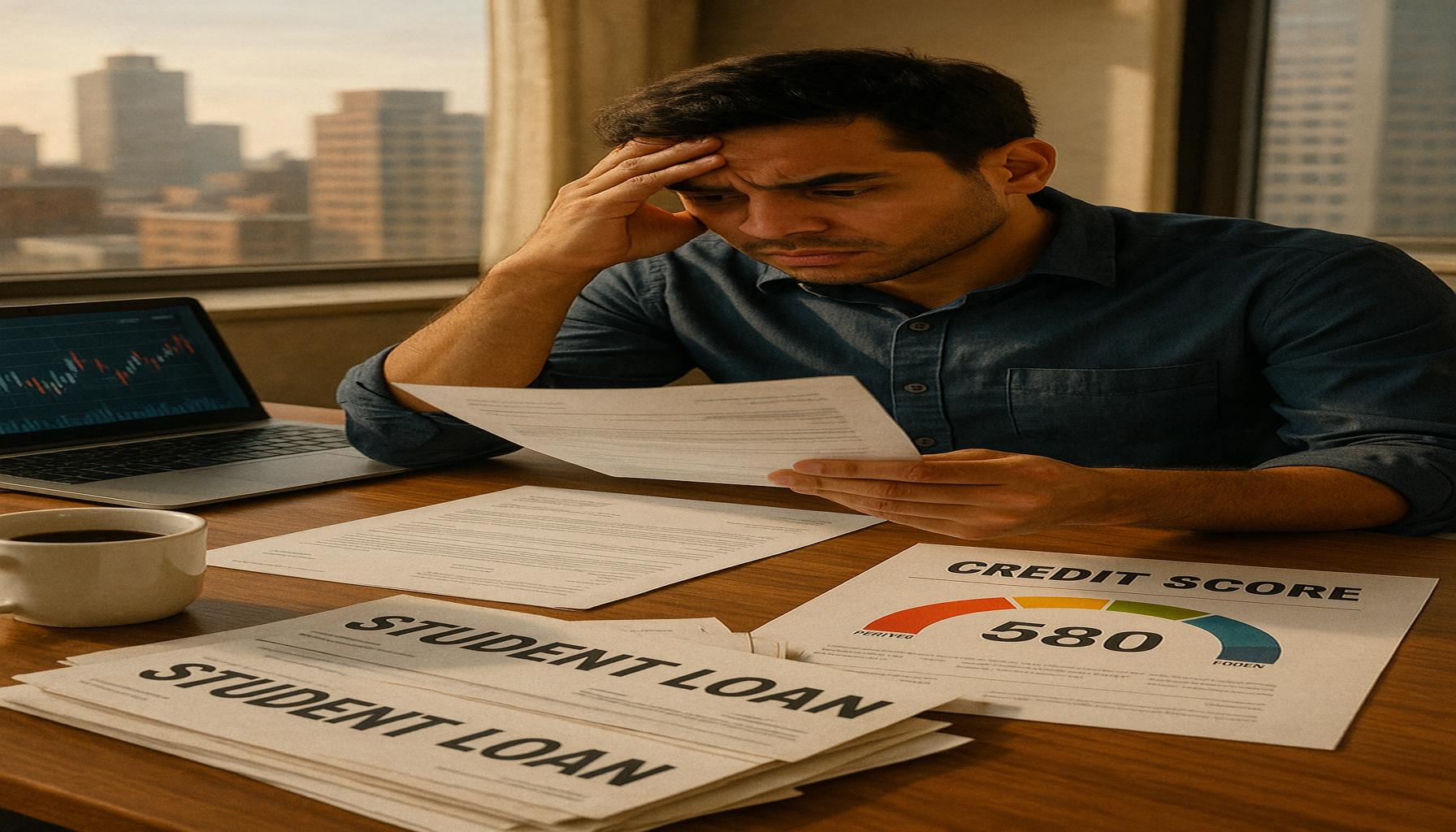

- Fair (580-659): Credit reports in this category may attract scrutiny, leading to less favourable loan conditions or, in some cases, flat-out denial for credit applications.

- Poor (below 580): A score in this range could severely limit financial options. Young adults may struggle to secure necessary loans, impacting long-term financial wellness.

Moreover, most lenders in New Zealand also consider the credit utilization ratio, which is the ratio of outstanding credit card balances to total credit limits. Experts recommend keeping this ratio below 30%. For example, if a young adult has a credit limit of $10,000, they should ideally maintain a balance below $3,000 to foster a positive credit score. This strategy not only bolsters credit ratings but provides flexibility for managing unforeseen expenses.

Understanding the impact of credit extends into practical applications as well. Situations such as applying for a rental property or attempting to secure a car loan highlight the tangible effects of credit scores. Landlords often assess applicants’ credit histories to gauge whether they can trust them to meet rental obligations. In cities with competitive rental markets such as Auckland or Wellington, having a favorable credit score can be a distinct competitive advantage, ensuring access to more desirable living arrangements.

It is also essential for young individuals to familiarize themselves with various credit products available in New Zealand. Common options include:

- Credit Cards: Offering flexibility and rewards, these can also lead to debt if not managed properly. Using them prudently involves maintaining low balances and timely payments.

- Personal Loans: Suitable for larger purchases, they require careful consideration of interest rates and repayment terms to avoid exacerbating debt.

- Student Loans: An investment in education, these loans generally have lower interest rates; however, graduates must handle repayments responsibly to maintain credit health moving forward.

In conclusion, young adults in New Zealand are in a unique position to harness the power of credit for their financial benefit. Understanding credit, building a solid history, and managing financial products effectively can lay the groundwork for a stable and prosperous future. As financial literacy continues to evolve, equipping oneself with this knowledge becomes paramount to navigating the complexities of modern-day financial landscapes.

CHECK OUT: Click here to explore more

Financial Independence and Credit as a Tool

The journey towards financial independence is a crucial phase for young adults in New Zealand, and credit plays an instrumental role in achieving this milestone. The ability to use credit wisely can lead to establishing a strong financial foundation that supports various life goals, including homeownership and investment opportunities.

One key benefit of maintaining a healthy credit score is the prospect of homeownership. In New Zealand’s competitive property market, many young adults aspire to become first-time homeowners. With rising house prices, lenders have become increasingly cautious, and a solid credit score is imperative for securing a mortgage. For instance, a first-time buyer with a credit score above 700 may qualify for lower interest rates, which can save them tens of thousands of dollars over the life of the mortgage. In contrast, individuals with lower scores may face higher rates, further complicating their ability to enter the housing market.

Furthermore, credit can influence not only the costs of borrowing but also access to further financial products that can enhance financial literacy and management. For example, young adults with a good credit history are often more likely to be approved for a revolving line of credit, which can serve as a safety net during unexpected financial challenges. This flexibility allows for crucial emergency funding while providing an opportunity to maintain or improve credit scores when managed responsibly.

Investment opportunities also arise from a solid credit profile. Young adults who have demonstrated responsible credit usage may find it easier to secure personal loans for investment purposes, such as purchasing shares or investing in a small business. For instance, a young entrepreneur looking to start a business may secure a loan at a favourable interest rate, whereas someone with a poor credit score may face rejections or exorbitant rates that hinder their entrepreneurial ambitions.

Moreover, service providers across various sectors—ranging from utility companies to mobile network providers—often conduct credit checks before offering services. A positive credit history increases the chances of qualifying for deposits waived or accessing premium services. This can significantly enhance lifestyle choices and conveniences, allowing young adults to avoid upfront costs that can strain already limited budgets.

While understanding the importance of credit is crucial, financial education is equally significant. It is essential for young adults in New Zealand to engage with resources that build their understanding of credit. Various organisations and financial advisors offer seminars and workshops aimed at demystifying the complexities of credit scores, financial planning, and responsible borrowing. Emerging digital tools also facilitate monitoring credit scores and financial health, empowering users to take control of their fiscal futures.

Credit cards, when used judiciously, offer an excellent way for young adults to build their credit history. However, caution is indispensable given that misuse can lead to spiralling debt. The Statistics New Zealand ‘Household Income and Housing’ report estimates that over 50% of young adults are in some form of debt, highlighting the importance of understanding how to balance credit card usage with income. Reward programs associated with credit cards can provide added benefits, ranging from cashback to travel points. Young adults should carefully assess the benefits and potential pitfalls, ensuring that their credit behaviours contribute positively to their financial narratives.

Ultimately, a sound understanding and strategic use of credit can pave the way for young adults in New Zealand to not only achieve financial stability but also to thrive in an increasingly complex economic landscape. By making informed decisions about credit, young individuals can unlock opportunities that enhance their quality of life while securing their financial future.

SEE ALSO: Click here to read another article

Conclusion

In conclusion, the significance of credit for young adults in New Zealand cannot be overstated. A solid understanding and responsible management of credit not only facilitate immediate financial needs but also pave the way for long-term aspirations such as homeownership, entrepreneurship, and investment opportunities. With the New Zealand housing market becoming increasingly competitive, maintaining a healthy credit score is vital for securing favourable mortgage rates and overcoming barriers to entry. Moreover, a positive credit history enhances access to essential services and financial products, equipping young individuals with the tools necessary to navigate unforeseen financial challenges.

As young adults embark on their journey towards independence, they must prioritise financial education. Engaging with workshops and digital resources will empower them to make informed decisions about their credit behaviours and financial management. Understanding the implications of credit card usage and effectively balancing credit with income are crucial, particularly when considering that a significant portion of young adults are currently in debt.

Ultimately, credit serves as a powerful instrument that, when used wisely, can open doors to improved quality of life and secure a stable financial future. By cultivating informed credit practices and integrating sound financial education into their lives, young adults in New Zealand can confidently set themselves on a path to achieving their financial goals and aspirations. With diligence and awareness, they can harness the benefits of credit to create a prosperous economic landscape in their personal lives.