The Common Mistakes That Affect Your Credit Score

Understanding the Impact of Your Credit Score

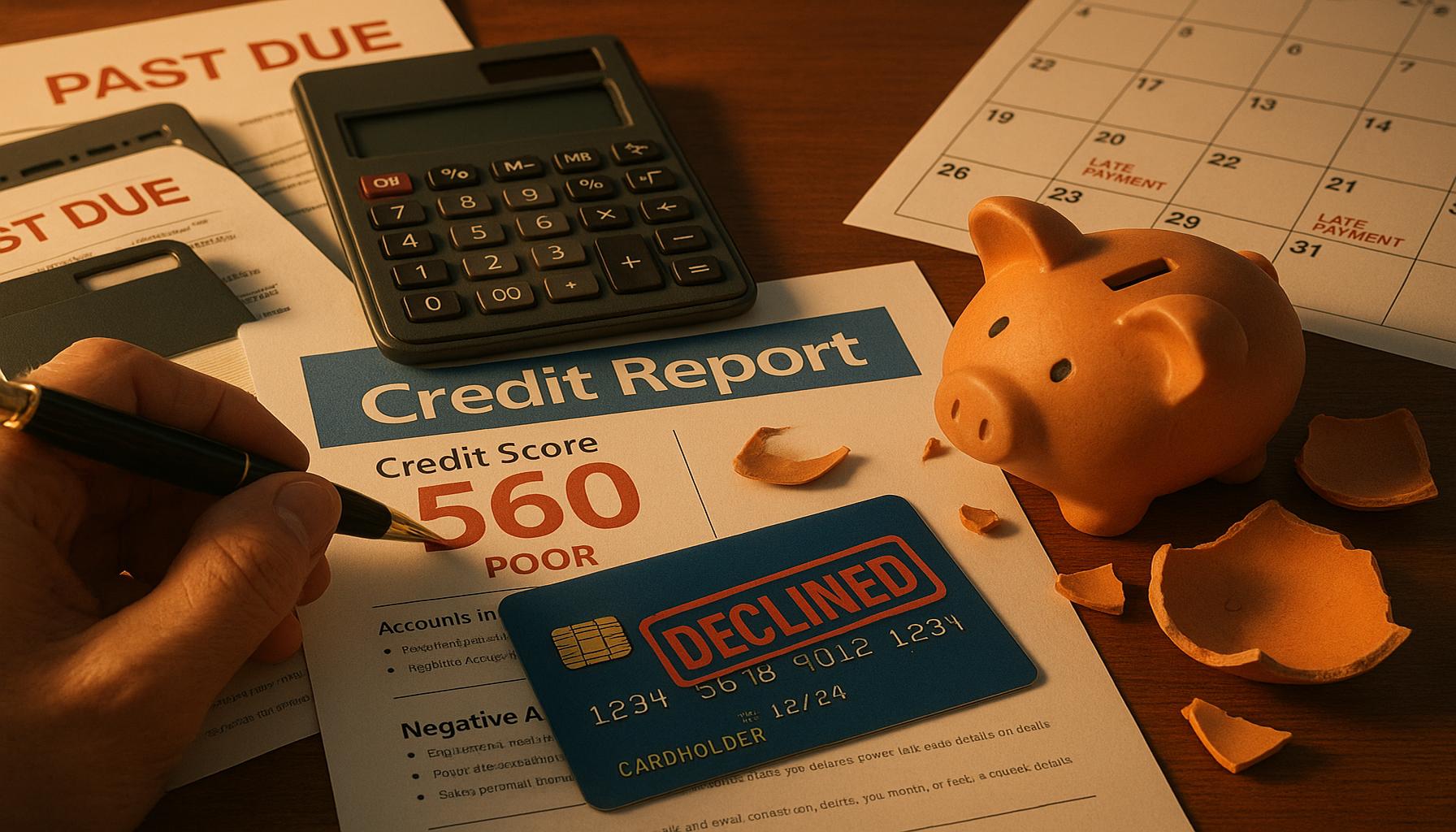

Your credit score is more than just a number; it is a vital indicator of your financial health. In New Zealand, where lending criteria can be stringent, this score can significantly affect your ability to secure loans for major purchases such as homes and vehicles, as well as influence interest rates and insurance premiums. Having a strong credit score can mean the difference between receiving a competitive loan offer or being denied altogether.

Unfortunately, many individuals make unintentional errors that can adversely affect their credit scores. It’s crucial to recognize these errors to protect your financial future. Below, we explore several common pitfalls people encounter, along with insights on how to avoid them:

- Missing Payments: One of the most detrimental actions is failing to make payments on time. Even a single late payment can lower your score, as payment history accounts for approximately 35% of your credit score. In New Zealand, missed payments can stay on your credit report for up to five years, making it imperative to establish reminders or automate payments to stay on track.

- High Credit Utilisation: Utilising over 30% of your available credit can pose problems for your credit score. For example, if your credit limit is NZD 10,000, maintaining a balance above NZD 3,000 could indicate risky financial behavior to lenders. To optimize your credit score, keep your utilisation below this threshold and aim for as low as 10% if possible.

- Closing Old Accounts: While it may seem beneficial to close accounts you no longer use, especially those with high fees, doing so can shorten your credit history length. A longer credit history can enhance your score, as it demonstrates a track record of responsible credit management. Consider keeping these accounts open, especially if they have no annual fees, to maintain your credit history.

- Ignoring Credit Reports: Regularly checking your credit report is essential. In New Zealand, you are entitled to request a free report from major credit reporting agencies annually. This proactive measure allows you to spot and rectify errors, such as incorrect payment histories or mixed files, before they negatively impact your score.

- Applying for Multiple Credits: Multiple applications for credit in a short period can create a red flag for lenders, suggesting financial distress. In New Zealand, every credit inquiry can drop your score slightly. To maintain a healthy score, limit applications and focus on researching products that are the best fit for your financial situation.

Being aware of these common mistakes is essential, particularly in New Zealand’s unique financial context. Understanding the implications of your financial actions can empower you to make more informed decisions. By actively managing your credit and avoiding these pitfalls, not only can you prevent negative consequences, but you can also lay a strong foundation for enhanced financial health and greater economic opportunities.

CHECK OUT: Click here to explore more

Common Pitfalls That Damage Your Credit Score

In order to maintain a healthy credit score, it is fundamental to avoid certain mistakes that can lead to significant setbacks. Oftentimes, individuals may not realize how their daily financial behaviors influence their credit ratings. Below, we delve into further detail on some of these common mistakes and provide actionable strategies to mitigate their effects:

- Exceeding Your Credit Limit: While it may seem harmless to temporarily exceed your credit limit, the repercussions on your credit score can be severe. In New Zealand, going beyond your credit cap can trigger fees and negatively impact your credit utilisation ratio. This ratio is critical as it comprises about 30% of your credit score. Staying well within your limits not only helps you avoid costly penalties but also presents you as a responsible borrower.

- Not Diversifying Your Credit: Having a mix of credit accounts, such as credit cards, personal loans, and mortgages, can enhance your credit score. This variety demonstrates to potential lenders that you can handle different types of credit responsibly. In contrast, relying solely on one type of credit may limit your score. Strive for diversification, but ensure that you manage all your accounts diligently to avoid negative impacts.

- Neglecting To Address Identity Theft: With the rise of digital fraud, identity theft has become increasingly prevalent. If fraudulent accounts or activities are linked to your credit report, this can lead to a significant decrease in your score. It’s crucial to regularly monitor your credit report for suspicious activities and report any discrepancies immediately. In New Zealand, consumers are protected under laws that allow them to contest inaccuracies on their credit file, so act promptly if you suspect fraud.

- Using Only One Credit Card: Many individuals make the mistake of limiting themselves to a single credit card for all transactions. While this may simplify tracking expenses, it can inadvertently lead to high credit utilisation and missed payment issues. Consider using multiple cards judiciously to optimize your credit score while keeping each card’s balance low. Using a mix of cards effectively can also yield better rewards and cashback benefits.

- Overlooking Small Debts: Sometimes, minor debts, such as parking fines or energy bills, may slip through the cracks. However, these debts can end up in collections and severely affect your credit score. It’s essential to stay aware of all your obligations, regardless of size, and address them promptly. Set reminders for payment deadlines or automate payments whenever possible to prevent any adverse effects.

Recognizing these common mistakes is a step towards improving your credit profile. The importance of cultivating good credit management habits cannot be overstated, particularly in New Zealand’s competitive financial landscape. By actively engaging with your finances and making informed decisions, you can significantly enhance your credit score and secure a better financial future.

CHECK OUT: Click here to explore more

Additional Factors Contributing to Credit Score Decline

To further elucidate the landscape of credit management, it is imperative to explore additional mistakes that can impede the health of your credit score. Understanding how these factors interrelate and affect your financial standing is crucial for making prudent financial decisions. Below are several more pitfalls to avoid:

- Failing to Keep Old Credit Accounts Open: One of the key components that contribute to your credit history length is the age of your accounts. Closing old credit accounts, even if they are not in use, can shorten your credit history and potentially lower your score. Research shows that longer credit histories are advantageous to your overall score as they demonstrate a track record of responsible borrowing. If you have older accounts that are in good standing, it may be beneficial to keep them open, especially if they have no annual fees.

- Missing Payment Due Dates: A single missed payment can have a disastrous impact on your credit score, potentially dropping it by as much as 100 points, depending on your overall credit history. Payment history constitutes about 35% of your credit score, making it the most influential factor. To avoid late payments, consider scheduling alerts for due dates or utilizing automatic payments for recurring bills. For New Zealand consumers, many banks offer services that send reminders via text or email, which can aid in timely payments.

- Frequently Opening New Credit Accounts: While diversifying your credit can be beneficial, opening too many new accounts in a short period can be perceived negatively by lenders. Each application for credit typically results in a hard inquiry on your credit report, which can temporarily decrease your score. A flurry of recent inquiries may signal to lenders that you are in financial distress. Aim to space out credit applications and only apply for new accounts when absolutely necessary.

- Ignoring Your Credit Report: Failing to regularly check your credit report can lead to missed errors or inaccuracies that can harm your credit score. Credit reports in New Zealand are available for free once a year from major credit bureaus. Taking the time to review your report for mistakes can help you identify areas for improvement, and more importantly, notify you of any fraudulent activity. Additionally, knowing your credit report allows you to be proactive in correcting errors that may negatively impact your financial standing.

- Not Utilizing Credit Responsibly: It’s not only about how much credit you have but how you use it. For example, many borrowers fall into the trap of using credit cards to their maximum limits without paying them off promptly. This high credit utilization ratio – ideally kept below 30% – can be detrimental to your score. Aim to maintain lower balances on your credit cards and make it a habit to pay off outstanding amounts each month. Furthermore, optimizing your credit usage can hinge on strategically planning your expenses, utilizing credit for larger purchases while maintaining adequate savings for repayment.

By being cognizant of these additional factors, individuals can better navigate the complexities of credit management. A holistic understanding of how each component can impact your credit score allows for informed, responsible financial choices that greatly contribute to long-term financial health. In New Zealand’s competitive lending environment, taking proactive measures ensures that you maintain a strong credit score capable of unlocking better opportunities in the future.

CHECK OUT: Click here to explore more

Conclusion

As we have detailed throughout this exploration of credit management, understanding the common mistakes that affect your credit score is essential for maintaining a healthy financial profile. From neglecting payment deadlines to the perils of closing old credit accounts, each misstep showcases how seemingly minor oversights can significantly impact your creditworthiness. Crucially, it’s evident that a single negative event, such as a missed payment, can lead to drastic short-term declines in your score; however, informed management of one’s credit can yield substantial long-term benefits.

In New Zealand, where competition among lenders remains high, the advantages of a solid credit score cannot be overstated. A robust credit score opens doors to better rates, favorable terms, and enhanced borrowing options. Regularly reviewing your credit report for inaccuracies and understanding the importance of credit utilization are not just best practices—they are vital strategies to foster financial health. Furthermore, taking proactive measures, such as setting reminders for payment due dates and planning prudent financial behaviors, will contribute to building and sustaining an impressive credit score.

In summary, by avoiding common pitfalls and actively engaging in responsible credit management, individuals can not only protect but also enhance their financial standing. Ultimately, this deliberate approach to credit can provide the necessary leverage for securing optimal lending opportunities and achieving future financial goals.