Impact of Credit Card Use on Financial Health

Understanding Credit Cards: A Double-Edged Sword in Personal Finance

The prevalence of credit cards in New Zealand underscores their significance in daily financial activities, with studies indicating that over 50% of New Zealanders possess at least one credit card. The popularity of these financial tools is not without reason, as they offer numerous benefits that can enhance personal financial management. However, it is essential to weigh these advantages against the inherent risks to ensure a balanced financial approach.

Advantages of Credit Cards

Credit cards provide a plethora of advantages that can foster both convenience and rewards for users.

- Convenience: Credit cards present an effortless means to access funds for everyday purchases, whether it’s groceries, gas, or online shopping. For instance, making a payment using a contactless card at a local supermarket saves time and enhances the shopping experience.

- Rewards programs: Many credit cards offer enticing rewards programs that can significantly benefit users. From earning cash back on transactions to accumulating points for travel or shopping, these benefits can contribute to saving money or enhancing lifestyle experiences. For example, a card that offers air miles can be particularly advantageous for frequent travelers, allowing them to earn free flights or upgrades on their journeys.

- Building credit history: When used responsibly, credit cards can help individuals build a positive credit history, which is crucial for future financial endeavors, such as applying for a mortgage or personal loan. Regular, on-time payments can enhance one’s credit score, making it easier to secure favorable interest rates down the line.

Risks of Credit Card Usage

Despite their benefits, credit cards carry significant risks that can jeopardize financial stability if not managed wisely.

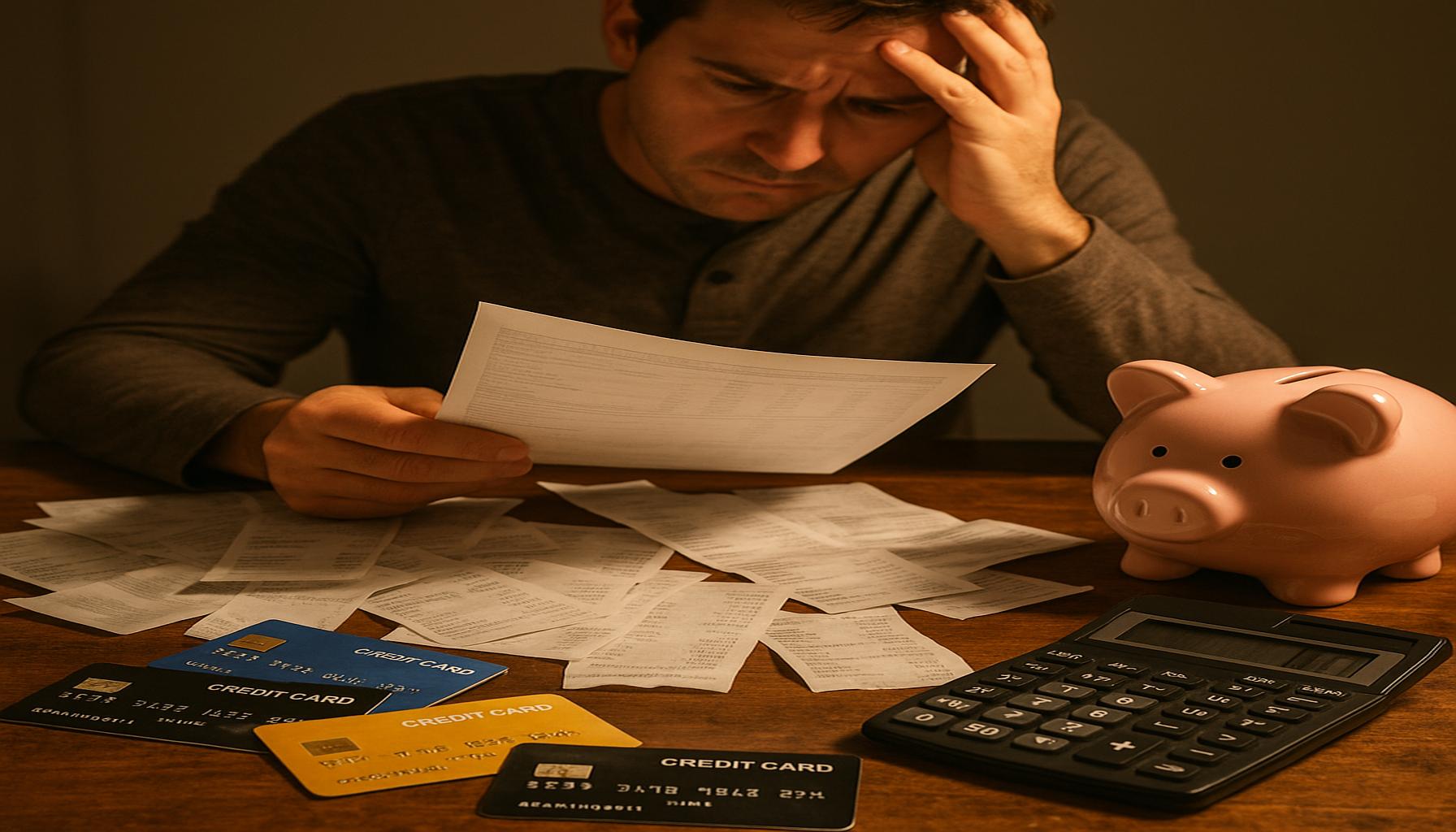

- Debt accumulation: The allure of credit cards can lead to overspending, resulting in high-interest debt that may spiral out of control. For example, if one has a balance of $5,000 with an interest rate of 20%, failing to pay the full amount each month can result in accruing over $1,000 in interest charges within a year.

- Negative credit impact: Late or missed payments can severely damage an individual’s credit rating. In New Zealand, payment history accounts for a significant portion of the credit score, meaning that even a single overlooked payment can have long-lasting effects on one’s financial reputation.

- Overspending tendency: The ease of using credit cards can encourage impulsive purchases, leading to financial strain. For example, a night out with friends can quickly turn into an unplanned expense if the credit card is relied upon without a budget in place.

Navigating Credit Card Use in New Zealand

Late payment fees and interest rates in New Zealand can profoundly influence an individual’s overall financial health. It is crucial for cardholders to familiarize themselves with their card’s terms and conditions, including fees associated with missed payments or exceeding credit limits. The Reserve Bank of New Zealand often analyzes credit card debt trends, highlighting the importance of maintaining a reliable repayment strategy to avoid falling into a debt trap.

Ultimately, navigating credit card use requires a well-thought-out strategy. By understanding the balance between leveraging credit for rewards and safeguarding against potential pitfalls, individuals can enjoy the benefits of credit cards while maintaining their financial well-being. Embracing informed practices—such as setting up automatic payments, utilizing budgeting apps, and regularly reviewing credit card statements—can lead to a healthier financial future.

CHECK OUT: Click here to explore more

The Balancing Act: Advantages and Drawbacks of Credit Card Use

In order to comprehend the impact of credit card use on financial health, it is essential to delve deeper into both the advantages and drawbacks that these financial tools present. Understanding these facets can help consumers make informed decisions about their credit card usage while effectively managing their overall financial situation.

Maximizing Financial Benefits Through Credit Cards

When used responsibly, credit cards can serve as valuable instruments for managing personal finances, provided users are aware of how to maximize their benefits. Several strategies can help cardholders extract the utmost value from their credit cards:

- Smart payment strategies: Utilizing strategies such as the “pay in full” method can prevent consumers from accruing high-interest debt. By paying off the monthly balance entirely before the due date, individuals can take advantage of the grace period on new purchases, thus avoiding interest charges entirely.

- Utilizing rewards optimally: Selecting a credit card that aligns with personal spending habits can amplify rewards. For instance, if a user frequently travels, a card offering travel rewards would be advantageous. Additionally, understanding the fine print of rewards programs—such as expiration dates and spending thresholds—can aid in maximizing these benefits.

- Monitoring credit utilization: Maintaining a low credit utilization ratio, typically below 30%, is crucial for a healthy credit score. By keeping balances low relative to credit limits, users can enhance their creditworthiness, which can lead to more favorable terms on loans and lower interest rates in the future.

Understanding the Detrimental Effects of Mismanagement

Conversely, mismanagement of credit cards poses significant risks that can adversely impact individuals’ financial well-being. Among the most pressing concerns are:

- Increased financial burden: Credit cards may lead to a cycle of debt if users consistently charge more than they can repay. Excessive reliance on credit can culminate in unmanageable balances and high-interest costs that compound over time. For example, statistics indicate that nearly 30% of New Zealand credit card holders carry a balance month-to-month, suggesting many may struggle with paying off outstanding debts.

- Psychological stress: The emotional toll of debt can interfere with daily life and decision-making. Stress associated with credit card debt can impact mental health and relationships, as financial obligations weigh heavily on individuals. Awareness of how credit card debt influences overall well-being is essential for peace of mind.

- Short-term vs. long-term consequences: While credit cards offer immediate access to funds, the long-term cost can be substantial. High-interest rates can lead to a cycle of continuous debt repayment, where users find themselves on the “minimum payment treadmill,” making little headway towards exiting the debt trap.

Consequently, a critical understanding of these advantages and drawbacks is essential for any individual using credit cards. By navigating through both sides of credit card usage, New Zealanders can develop a balanced approach that promotes financial health while mitigating risks associated with debt and mismanagement.

CHECK OUT: Click here to explore more

Long-term Financial Strategies: Navigating Credit Card Use Wisely

To further grasp the impact of credit card use on financial health, it is vital to consider long-term strategies that can aid consumers in maintaining their financial stability while leveraging the advantages of credit cards. By adopting a forward-thinking approach, individuals can enhance their financial literacy and resilience.

Building a Strong Credit History

One of the key aspects of responsible credit card use is the opportunity to build a robust credit history. A strong credit history is paramount, influencing everything from loan approvals to interest rates on mortgages. Below are strategies that can enhance creditworthiness:

- Consistent on-time payments: Making timely payments can significantly influence credit scores. According to Equifax New Zealand, payment history accounts for approximately 35% of credit scores. Setting up reminders or automatic payments can help ensure that no payments are missed.

- Limiting new credit inquiries: Frequent applications for new credit can negatively affect credit scores. It is important to be strategic about applying for new credit cards, involving careful consideration of one’s current financial standing and necessity for additional credit.

- Regular credit report checks: Monitoring credit reports for inaccuracies is essential. Consumers are entitled to one free credit report per year from various reporting agencies, which can reveal any discrepancies that could impact credit ratings. Correcting errors promptly can lead to improvements in financial standing.

The Role of Interest Rates in Credit Card Debt

Interest rates play a crucial role in determining the cost of carrying a credit card balance over time. Understanding how interest rates function can allow consumers to strategize accordingly:

- Comparison of rates: Different credit cards come with varying interest rates, which can significantly impact the total amount paid in interest over time. For instance, as of 2023, average credit card interest rates in New Zealand hover around 14% to 20%. Selecting a card with lower interest rates can save cardholders substantial amounts, particularly if they do not pay off their balance in full each month.

- Fixed vs. variable rates: It’s imperative to understand whether the credit card has a fixed or variable interest rate. While fixed rates provide predictability, variable rates can lead to higher costs if interest rates in the economy increase. Choosing the right type of rate is critical for long-term financial planning.

- Utilizing promotional rates wisely: Many credit cards offer promotional low or zero-interest rates for a limited time. These offers can serve as an effective way to pay down existing debt without accruing additional interest. However, consumers should be cautious of reverting to higher rates once the promotional period ends, often resulting in unexpected financial strain.

Creating an Emergency Fund

Establishing an emergency fund is a pivotal strategy that can mitigate the need for credit card reliance during financial emergencies. Here are key points to consider:

- Establishing a savings goal: Aiming for three to six months’ worth of living expenses can provide a financial cushion during unexpected events, such as loss of employment or medical emergencies. This approach minimizes the likelihood of utilizing credit cards for emergencies and accruing debt.

- Automatic savings plans: Automating transfers to a dedicated savings account can help build the emergency fund without requiring consistent effort. Seeing this fund grow can also instill a sense of financial security, reducing the impulse to rely on credit cards.

By focusing on long-term strategies such as building a strong credit history, understanding interest rates, and creating emergency funds, consumers can engage with credit cards in a manner that promotes financial health and empowers them to make informed financial decisions.

SEE ALSO: Click here to read another article

Conclusion: Understanding the Financial Landscape of Credit Card Use

The impact of credit card use on financial health is multifaceted, intertwining both potential benefits and risks. As discussed, responsible credit card management is indispensable for building a strong credit history, which in turn influences future borrowing capabilities and financial opportunities. By prioritizing strategies such as consistent on-time payments and regular credit report checks, individuals can significantly bolster their credit profiles and avoid the pitfalls of accumulating debt.

Furthermore, the awareness of interest rates—whether fixed or variable—is essential in navigating the costs associated with credit card balances. Selectively choosing credit cards with lower rates or utilizing promotional offers can yield considerable savings, thus contributing to a healthier financial status. However, consumers must approach these offers cautiously to avert potential financial strain when introductory rates expire.

Moreover, establishing an emergency fund is a critical aspect of financial planning that not only provides a buffer during unexpected situations but also lessens the reliance on credit cards. By setting specific savings goals and employing automatic savings strategies, individuals can cultivate a sense of security that protects them against unforeseen expenses.

In conclusion, the impact of credit card use on financial health necessitates a proactive and informed approach. By embracing sound financial practices, consumers in New Zealand can harness the advantages of credit cards while safeguarding their financial future, ultimately leading to a more stable and empowered financial life.